Payback Period Analysis: Project Economics Engineering Guide

Calculate simple and discounted payback periods, evaluate investment criteria using NPV and IRR, and understand time value of money for pipeline and midstream project justification.

Payback period is the time required for cumulative cash inflows from a project to equal the initial investment. It is one of the most widely used screening tools in capital budgeting for pipeline and midstream projects.

Pipeline expansions

Capacity additions

New compressor stations, looping, diameter increases justified by throughput revenue.

Efficiency projects

Energy savings

VFDs, insulation upgrades, heat recovery systems with utility cost reduction.

Reliability improvements

Maintenance reduction

Equipment upgrades that reduce downtime and maintenance costs.

Safety & compliance

Risk mitigation

Integrity management, leak detection, safety systems justified by avoided costs.

Key Concepts

Initial investment (I₀): Total capital expenditure including equipment, installation, engineering, and startup costs

Cash flow (CF): Net annual cash inflow from project (revenue increase or cost savings minus operating costs)

Time value of money: Principle that a dollar today is worth more than a dollar in the future due to earning potential

Discount rate (r): Required rate of return reflecting risk and cost of capital

Why payback analysis matters: Simple payback provides quick go/no-go screening. Discounted payback accounts for time value of money. Combined with NPV and IRR, these metrics form a comprehensive investment decision framework.

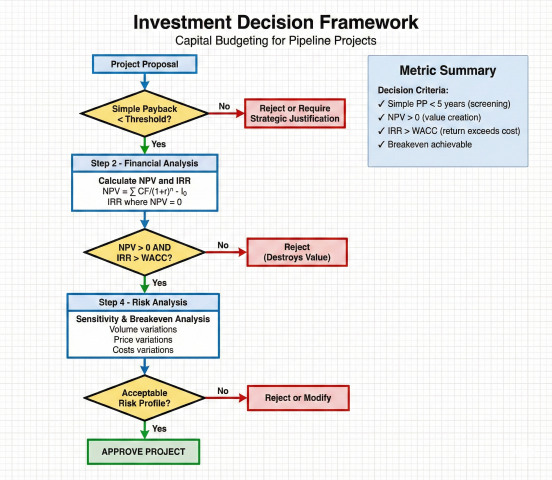

Investment decision framework integrating payback period screening with NPV, IRR, and risk analysis for capital project evaluation

Advantages of Payback Method

Simplicity: Easy to calculate and explain to non-financial stakeholders

Risk indicator: Shorter payback means faster capital recovery and lower risk

Liquidity focus: Emphasizes cash recovery important for capital-constrained companies

Screening tool: Quick filter for obviously poor projects before detailed analysis

Limitations of Payback Method

Ignores cash flows beyond payback: Doesn't consider project life or total profitability

No time value (simple): Simple payback doesn't discount future cash flows

Arbitrary cutoff: Payback threshold (e.g., 3 years) may not align with value creation

Biased against long-term projects: May reject valuable long-lived infrastructure

2. Simple Payback Period

Simple payback period is the most basic capital budgeting metric. It calculates the time to recover initial investment assuming equal annual cash flows, without considering time value of money.

When cash flows vary by year, calculate cumulative cash flow and find when it equals initial investment:

Cumulative Cash Flow Method:

Cumulative CF_n = Σ(CF₁ + CF₂ + ... + CF_n)

Find n where Cumulative CF_n ≥ I₀

If recovery occurs partway through year n:

PP = (n-1) + (I₀ - Cumulative CF_(n-1)) / CF_n

Example with varying cash flows:

Initial investment: $800,000

Year 1: $150,000 → Cumulative: $150,000

Year 2: $200,000 → Cumulative: $350,000

Year 3: $250,000 → Cumulative: $600,000

Year 4: $300,000 → Cumulative: $900,000

Recovery occurs in Year 4:

Remaining after Year 3: $800,000 - $600,000 = $200,000

Fraction of Year 4: $200,000 / $300,000 = 0.67

Payback Period = 3 + 0.67 = 3.67 years

Typical Payback Thresholds by Industry

Project Type

Typical Threshold

Rationale

Energy efficiency (motors, VFDs)

2-3 years

Technology obsolescence, short economic life

Process improvements

3-5 years

Moderate risk, proven technology

Pipeline capacity expansion

4-7 years

Long-term contracts, regulated returns

New facilities (greenfield)

5-10 years

30+ year design life, strategic infrastructure

Safety/environmental compliance

Not applicable

Mandatory; justify via risk reduction, not payback

R&D / pilot projects

N/A or 1-2 years

High uncertainty; very short payback or strategic value

Pipeline Expansion Example

A pipeline operator considers adding a compressor station to increase throughput from 500 MMcf/d to 650 MMcf/d.

Project Data:

Compressor station cost: $12,000,000

Additional throughput: 150 MMcf/d

Transportation tariff: $0.50/Mcf

Operating days: 350 days/year

Annual O&M cost: $1,200,000/year

Annual Revenue Increase:

Volume = 150,000 Mcf/day × 350 days = 52,500,000 Mcf/year

Revenue = 52,500,000 × $0.50 = $26,250,000/year

Net Annual Cash Flow:

CF = $26,250,000 - $1,200,000 = $25,050,000/year

Simple Payback:

PP = $12,000,000 / $25,050,000 = 0.48 years = 5.8 months

Interpretation: Very attractive project with sub-1-year payback, assuming capacity can be sold.

Energy Efficiency Example

Replace existing fixed-speed compressor motor with VFD to reduce power consumption:

Project Data:

VFD installed cost: $85,000

Current power consumption: 400 kW average

Expected reduction: 15%

Power cost: $0.10/kWh

Operating hours: 8,000 hr/year

Annual Energy Savings:

kWh saved = 400 kW × 0.15 × 8,000 hr = 480,000 kWh/year

Cost savings = 480,000 × $0.10 = $48,000/year

Simple Payback:

PP = $85,000 / $48,000 = 1.77 years

Interpretation: Acceptable payback for energy efficiency. Project likely approved.

Rule of thumb: For midstream operators, simple payback < 3 years is considered excellent, 3-5 years is good, 5-7 years is marginal. Projects > 7 years require strategic justification beyond financial return.

Cumulative cash flow curve illustrating payback period where cumulative returns equal initial investment

3. Discounted Payback Period

Discounted payback period accounts for the time value of money by discounting future cash flows to present value. This provides a more conservative and financially rigorous assessment than simple payback.

Present Value of Cash Flows

Present Value Formula:

PV = CF / (1 + r)ⁿ

Where:

PV = Present value of cash flow ($)

CF = Future cash flow in year n ($)

r = Discount rate (decimal)

n = Year number

Cumulative Present Value:

Cumulative PV_n = Σ [CF_i / (1 + r)ⁱ] for i = 1 to n

Find n where Cumulative PV_n ≥ I₀

Discounted Payback Calculation

Step-by-Step Process:

1. Select appropriate discount rate (WACC or hurdle rate)

2. Calculate present value of each year's cash flow

3. Sum present values cumulatively by year

4. Find year when cumulative PV equals initial investment

5. Interpolate if recovery occurs mid-year

Interpolation Formula:

DPP = (n-1) + [(I₀ - Cumulative PV_(n-1)) / PV_n]

Where DPP = Discounted payback period (years)

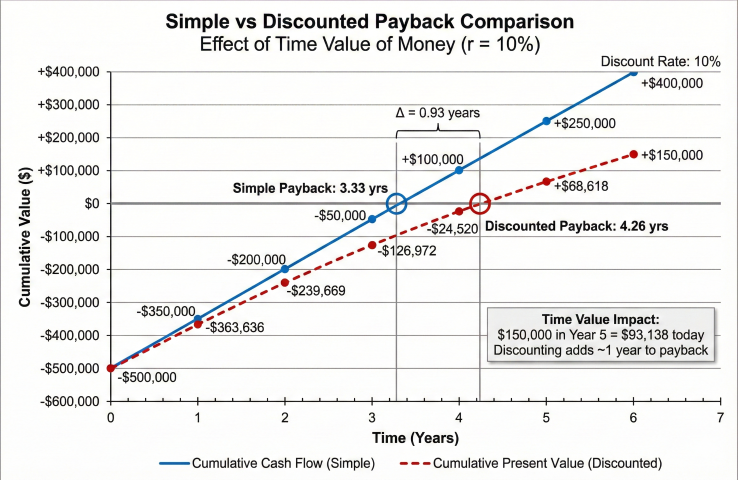

Comparison Example: Simple vs. Discounted Payback

Project with $500,000 initial investment, 10% discount rate:

Year

Cash Flow

Cumulative CF (Simple)

PV Factor (1+0.10)ⁿ

Present Value

Cumulative PV (Discounted)

0

-$500,000

-$500,000

1.000

-$500,000

-$500,000

1

$150,000

-$350,000

1.100

$136,364

-$363,636

2

$150,000

-$200,000

1.210

$123,967

-$239,669

3

$150,000

-$50,000

1.331

$112,697

-$126,972

4

$150,000

$100,000

1.464

$102,452

-$24,520

5

$150,000

$250,000

1.611

$93,138

$68,618

Simple Payback Calculation:

Recovery in Year 4: 3 + ($50,000 / $150,000) = 3.33 years

Discounted Payback Calculation:

Recovery in Year 5: 4 + ($24,520 / $93,138) = 4.26 years

Difference: 4.26 - 3.33 = 0.93 years longer

Interpretation: Discounting increases payback by ~1 year due to time value of money.

The $150,000 received in Year 5 is worth only $93,138 today.

Selecting the Discount Rate

The discount rate should reflect the project's risk and opportunity cost of capital:

Discount Rate Type

Typical Range

When to Use

WACC (Weighted Average Cost of Capital)

8-12%

Standard projects with average risk profile

Hurdle rate (WACC + risk premium)

12-18%

High-risk projects, new technologies, uncertain markets

Weighted Average Cost of Capital:

WACC = (E/V) × Re + (D/V) × Rd × (1 - Tc)

Where:

E = Market value of equity

D = Market value of debt

V = E + D (total value)

Re = Cost of equity

Rd = Cost of debt

Tc = Corporate tax rate

Example Calculation:

Equity: $100M at 12% cost

Debt: $40M at 6% cost

Tax rate: 25%

E/V = $100M / $140M = 71.4%

D/V = $40M / $140M = 28.6%

WACC = 0.714 × 12% + 0.286 × 6% × (1 - 0.25)

WACC = 8.57% + 1.29% = 9.86% ≈ 10%

Impact of discount rate: Higher discount rates penalize distant cash flows more heavily, increasing discounted payback period. A 5% increase in discount rate typically adds 0.5-1.5 years to payback for 5-10 year projects.

Simple vs discounted payback comparison showing how time value of money extends payback period by approximately one year at 10% discount rate

When Projects Never Pay Back

Some projects have negative NPV and never achieve discounted payback:

Example of No Payback:

Initial investment: $1,000,000

Annual cash flow: $80,000/year for 20 years

Discount rate: 12%

PV of cash flows = $80,000 × [PV annuity factor, 12%, 20 years]

PV = $80,000 × 7.469 = $597,520

Since $597,520 < $1,000,000, project never pays back in PV terms.

NPV = -$1,000,000 + $597,520 = -$402,480 (reject project)

4. Breakeven Analysis

Breakeven analysis determines the minimum performance level (throughput, price, cost savings) required for a project to achieve target payback period or NPV = 0.

Breakeven Throughput

For capacity expansion projects, calculate minimum volume needed to recover investment:

Breakeven Volume Calculation:

Total Annual Cost = (I₀ / PP) + Annual O&M

Required Volume = Total Annual Cost / Unit Margin

Where:

I₀ = Initial investment

PP = Target payback period (years)

Unit Margin = Tariff revenue per unit - variable cost per unit

Example - Pipeline Looping:

Investment: $25,000,000

Target payback: 5 years

Annual O&M: $800,000/year

Tariff: $0.75/Mcf

Variable cost: $0.05/Mcf

Annual cost to recover = $25,000,000 / 5 + $800,000 = $5,800,000

Unit margin = $0.75 - $0.05 = $0.70/Mcf

Breakeven volume = $5,800,000 / $0.70 = 8,285,714 Mcf/year

= 22,710 Mcf/day (assuming 365 days)

If project adds 200 MMcf/d capacity and can sell 25 MMcf/d or more,

project exceeds breakeven requirement.

Breakeven Tariff/Price

Determine minimum price or tariff needed for acceptable economics:

Evaluate how payback period changes with key variables:

Scenario

Volume (MMcf/d)

Tariff ($/Mcf)

O&M ($/yr)

Annual CF

Payback (yrs)

Base Case

50

$0.80

$2.0M

$12.6M

3.97

Low volume (-20%)

40

$0.80

$2.0M

$9.68M

5.17

Low tariff (-15%)

50

$0.68

$2.0M

$10.41M

4.80

High O&M (+30%)

50

$0.80

$2.6M

$12.0M

4.17

Optimistic (all favorable)

60

$0.90

$1.8M

$17.91M

2.79

Pessimistic (all unfavorable)

40

$0.68

$2.6M

$7.33M

6.83

Assumes $50M investment, 365 operating days/year

Monte Carlo Simulation for Risk Assessment

For high-value projects, use probabilistic analysis to quantify payback period uncertainty:

Monte Carlo Approach:

1. Define probability distributions for uncertain variables:

- Volume: Normal distribution, mean 50 MMcf/d, std dev 8 MMcf/d

- Tariff: Triangular distribution, min $0.65, most likely $0.80, max $0.95

- O&M: Log-normal distribution, mean $2.0M, std dev $0.4M

2. Run 10,000 simulations, randomly sampling from distributions

3. Calculate payback period for each simulation

4. Analyze results:

- P10 (10th percentile): 3.1 years (optimistic)

- P50 (median): 4.2 years (expected)

- P90 (90th percentile): 6.8 years (pessimistic)

- Probability of payback < 5 years: 72%

5. Decision: Accept if P90 < management threshold (e.g., 7 years)

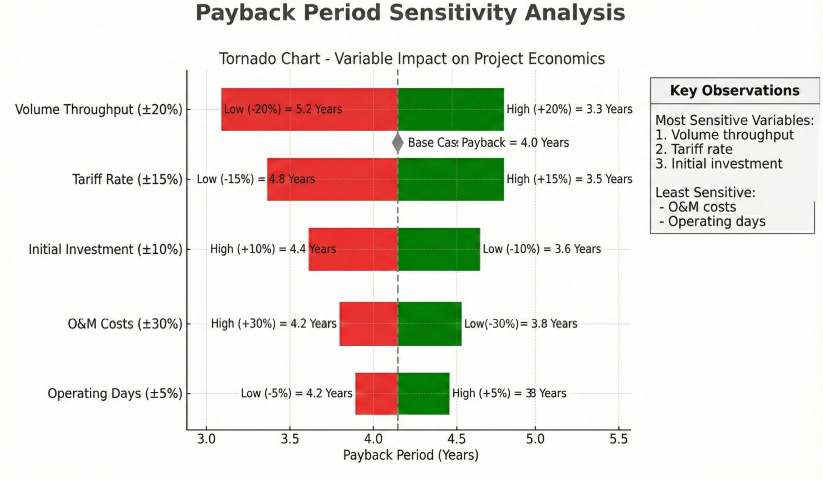

Sensitivity tornado chart identifying volume throughput and tariff rate as the most critical variables affecting payback period

5. Investment Decision Criteria

Payback period should be used alongside other financial metrics for comprehensive project evaluation. The primary criteria are Net Present Value (NPV) and Internal Rate of Return (IRR).

Communicate returns to management; compare to hurdle rates

Profitability Index

Measures value per dollar invested; good for capital rationing

Doesn't show absolute value; can conflict with NPV

Budget constraints; ranking projects with different scales

Profitability Index (PI)

Profitability Index Formula:

PI = PV of Future Cash Flows / Initial Investment

PI = [Σ (CF_t / (1+r)ᵗ)] / I₀

Decision Rule:

PI > 1.0 → Accept (NPV > 0)

PI < 1.0 → Reject (NPV < 0)

PI = 1.0 → Indifferent (NPV = 0)

Example:

PV of cash flows: $1,200,000

Investment: $1,000,000

PI = $1,200,000 / $1,000,000 = 1.20

Interpretation: Project returns $1.20 for every $1.00 invested (20% value creation)

Integrated Decision Framework

Comprehensive project evaluation using multiple criteria:

Project

Investment

Simple PP

Disc. PP

NPV @10%

IRR

PI

Decision

Compressor station

$8M

3.2 yr

4.1 yr

$3.5M

18.2%

1.44

Accept - All metrics favorable

VFD retrofit

$250K

2.8 yr

3.4 yr

$75K

24.5%

1.30

Accept - Excellent returns

Pipeline looping

$40M

6.5 yr

8.9 yr

$2.1M

11.8%

1.05

Marginal - Low but positive NPV

Meter upgrades

$1.2M

8.1 yr

Never

-$350K

7.2%

0.71

Reject - NPV < 0, IRR < WACC

SCADA system

$3M

N/A

N/A

-$1.2M

N/A

N/A

Accept - Safety/reliability, not financial

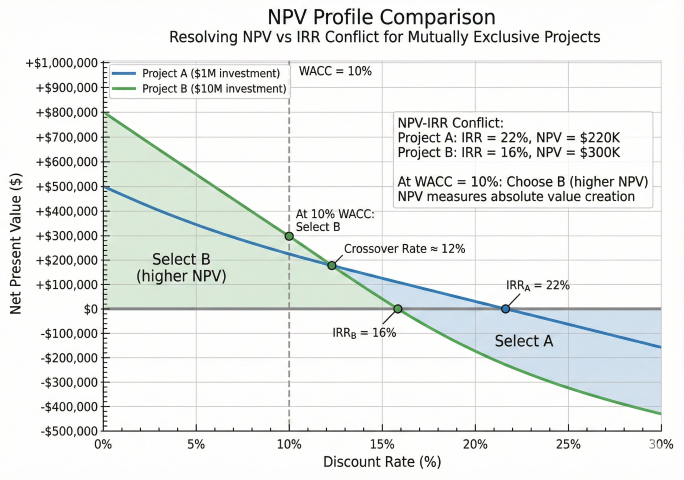

Decision Conflicts: NPV vs. IRR

For mutually exclusive projects of different scales, NPV and IRR can give conflicting rankings:

Example of NPV-IRR Conflict:

Project A (Small):

Investment: $1,000,000

NPV: $400,000

IRR: 22%

Project B (Large):

Investment: $10,000,000

NPV: $2,500,000

IRR: 16%

Analysis:

- By IRR: Select Project A (22% > 16%)

- By NPV: Select Project B ($2.5M > $0.4M)

Correct Decision: Select Project B

NPV measures absolute value creation. Project B adds $2.5M vs. $0.4M.

Even though A has higher percentage return, B creates more shareholder value.

When to use IRR: Comparing projects of similar scale and timing.

When to use NPV: Mutually exclusive projects of different scales (use NPV).

NPV profile crossover chart demonstrating how NPV and IRR can give conflicting rankings for mutually exclusive projects of different scales

Decision Tree for Project Approval

Recommended Decision Process:

Step 1: Calculate Simple Payback

- If PP > 10 years → Likely reject (unless strategic)

- If PP ≤ 3 years → Proceed to Step 2 (strong candidate)

- If 3 < PP ≤ 10 → Proceed to Step 2 (requires detailed analysis)

Step 2: Calculate NPV and IRR

- If NPV > 0 AND IRR > WACC → Accept

- If NPV < 0 OR IRR < WACC → Reject

- If NPV ≈ 0 → Sensitivity analysis required

Step 3: Sensitivity and Risk Analysis

- Identify key uncertainties (volume, price, costs)

- Calculate breakeven values

- Assess probability of achieving targets

- Consider strategic value, competitive position, regulatory factors

Step 4: Management Review

- Present all metrics with sensitivity cases

- Recommend accept/reject with rationale

- Identify key assumptions and risks

- Propose monitoring metrics for post-approval tracking

Best practice: Use simple payback for initial screening, NPV as primary decision criterion, IRR for communication to management, and discounted payback for risk assessment. No single metric tells the complete story.

What is the difference between simple payback and discounted payback period?+

Simple payback divides the initial investment by annual cash flow, ignoring the time value of money. Discounted payback uses present-valued cash flows, producing a longer and more accurate payback period. Discounted payback accounts for the opportunity cost of capital.

What is a typical acceptable payback period for midstream infrastructure projects?+

Midstream companies typically require a simple payback of 2-5 years and a discounted payback of 3-7 years, depending on risk and strategic importance. Pipeline projects with long-term contracts may accept longer paybacks, while wellhead compression typically requires payback under 2-3 years.

Why is payback period alone insufficient for investment decisions?+

Payback period ignores cash flows after the payback date, does not account for the time value of money (simple payback), and cannot compare projects with different cash flow patterns. It should be used alongside NPV and IRR for comprehensive investment evaluation.

How is breakeven analysis related to payback period calculations?+

Breakeven analysis determines the throughput volume, price, or utilization rate at which a project's revenues exactly equal its costs. Combined with payback analysis, it shows both when the investment is recovered and what minimum operating conditions are needed to achieve that recovery.