Evaluate pipeline and midstream project economics using NPV, IRR, and discounted cash flow analysis with WACC-based discount rates for capital investment decisions.

Net Present Value (NPV) analysis is the fundamental method for evaluating capital investments in pipeline and midstream projects. NPV quantifies project value by discounting future cash flows to present value using the company's cost of capital.

Time value of money

Present value concept

Dollar today worth more than dollar tomorrow due to earning potential and risk.

Investment decision

Accept if NPV > 0

Positive NPV means project returns exceed required return; creates value.

Ranking projects

Higher NPV preferred

Among mutually exclusive projects, select highest NPV option.

Capital budgeting

Portfolio optimization

Allocate limited capital to projects with highest NPV per dollar invested.

Key Financial Metrics

NPV (Net Present Value): Sum of discounted cash flows minus initial investment; measures absolute dollar value creation

IRR (Internal Rate of Return): Discount rate that makes NPV = 0; measures percentage return

PI (Profitability Index): NPV / Initial Investment; measures value per dollar invested

Payback Period: Years to recover initial investment (see payback-analysis-fundamentals.html)

WACC (Weighted Average Cost of Capital): Company's blended cost of debt and equity financing

Why NPV is preferred: NPV directly measures dollar value created, accounts for all cash flows, incorporates time value of money, and uses realistic discount rate (WACC). Superior to payback period or accounting rate of return for capital budgeting decisions.

NPV Decision Framework

NPV Result

Meaning

Decision

NPV > 0

Project returns exceed cost of capital

Accept - creates shareholder value

NPV = 0

Project returns equal cost of capital

Indifferent - no value creation/destruction

NPV < 0

Project returns below cost of capital

Reject - destroys shareholder value

NPV₁ > NPV₂

Mutually exclusive projects

Select Project 1 (higher NPV)

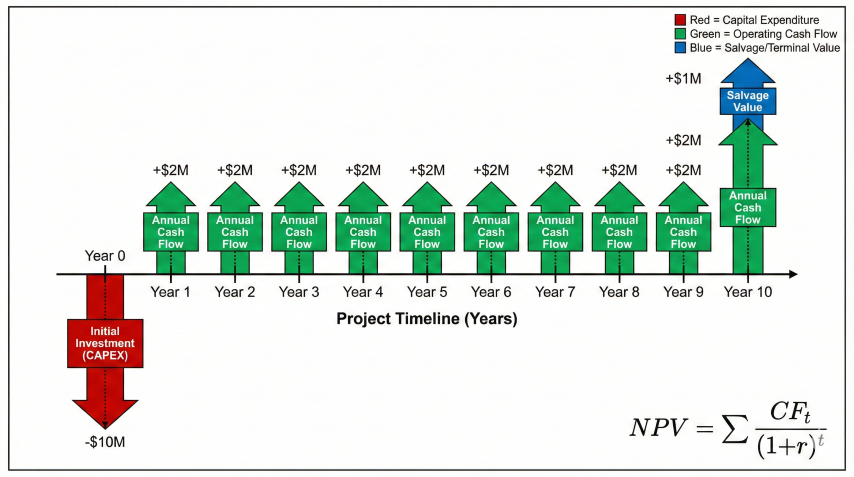

Types of Cash Flows

Project cash flow timeline illustrating initial investment, annual operating cash flows, and terminal salvage value used in NPV calculations.

Terminal cash flow (Year N): Salvage value, working capital recovery, decommissioning costs

Tax effects: Depreciation tax shield, capital gains/losses on disposal

Common Pipeline Investment Types

Project Type

Typical Investment

Cash Flow Profile

Project Life

Greenfield transmission pipeline

$500M - $5B

Large upfront CAPEX, stable long-term revenue

30-50 years

Lateral extension

$10M - $100M

Moderate CAPEX, incremental revenue

20-30 years

Compressor station upgrade

$20M - $200M

CAPEX, reduced fuel costs, increased capacity

15-25 years

Integrity/replacement

$5M - $50M

CAPEX, avoided failure costs, maintained revenue

10-20 years

Metering/automation

$1M - $10M

CAPEX, reduced labor, improved accuracy

10-15 years

2. NPV Calculation

NPV equals the sum of all future cash flows discounted to present value minus the initial investment.

NPV Formula

Net Present Value:

NPV = Σ [CF_t / (1 + r)^t] - Initial Investment

Or expanded:

NPV = -CF₀ + CF₁/(1+r)¹ + CF₂/(1+r)² + ... + CF_N/(1+r)^N

Where:

NPV = Net present value ($)

CF_t = Cash flow in year t ($)

r = Discount rate (WACC, decimal)

t = Time period (years)

N = Project life (years)

CF₀ = Initial investment (negative cash flow)

Alternative form with salvage value:

NPV = -I₀ + Σ(t=1 to N) [CF_t/(1+r)^t] + S_N/(1+r)^N

Where:

I₀ = Initial investment

S_N = Salvage value at end of year N

Discount Factor

Present Value Factor:

PV Factor = 1 / (1 + r)^t

This is the present value of $1 received in year t.

Example discount factors at r = 10%:

Year 1: PV = 1/1.10 = 0.9091 (each dollar worth $0.91 today)

Year 5: PV = 1/(1.10)^5 = 0.6209

Year 10: PV = 1/(1.10)^10 = 0.3855

Year 20: PV = 1/(1.10)^20 = 0.1486

Note: Distant cash flows heavily discounted (Year 20 dollar worth only $0.15 today)

IRR Definition:

Find IRR such that:

NPV = 0 = Σ [CF_t / (1 + IRR)^t] - I₀

For the lateral example above:

0 = -37 + 6/(1+IRR)¹ + 6/(1+IRR)² + ... + 6/(1+IRR)²⁰ + 5/(1+IRR)²⁰

Solve iteratively (trial and error or Excel IRR function):

IRR = 15.1%

Decision rule:

If IRR > WACC (15.1% > 10%), accept project ✓

If IRR < WACC, reject project

Note: IRR = 15.1% means project returns 15.1% annually,

exceeding 10% cost of capital by 5.1 percentage points.

Profitability Index

Profitability Index (PI):

PI = NPV / Initial Investment

Or:

PI = PV(Cash Inflows) / PV(Cash Outflows)

For lateral example:

PI = 14.82 / 37 = 0.40 = 40%

Interpretation: Every $1 invested creates $0.40 of value

Or: PV of inflows is 1.40× initial investment

Decision rule:

PI > 0: Accept (equivalent to NPV > 0)

PI < 0: Reject

Use for capital rationing: Rank projects by PI when budget limited

Unequal Cash Flows

Many projects have varying cash flows over time:

Example: Compressor Station with Increasing Tariffs

Year 0: CAPEX = -$50M

Year 1-5: CF = $8M/year

Year 6-10: CF = $10M/year (tariff increase)

Year 11-15: CF = $12M/year

Year 15: Salvage = $8M

Discount rate: r = 9%

Calculate NPV by summing discounted cash flows:

Years 1-5: PV = 8 × [(1-1.09^-5)/0.09] = 8 × 3.8897 = $31.12M

Years 6-10: PV = 10 × [(1-1.09^-5)/0.09] × (1.09)^-5 = 10 × 3.8897 × 0.6499 = $25.28M

Years 11-15: PV = 12 × [(1-1.09^-5)/0.09] × (1.09)^-10 = 12 × 3.8897 × 0.4224 = $19.72M

Salvage: PV = 8 / (1.09)^15 = 8 × 0.2745 = $2.20M

NPV = -50 + 31.12 + 25.28 + 19.72 + 2.20 = $28.32M ✓

Project highly attractive with NPV = $28M

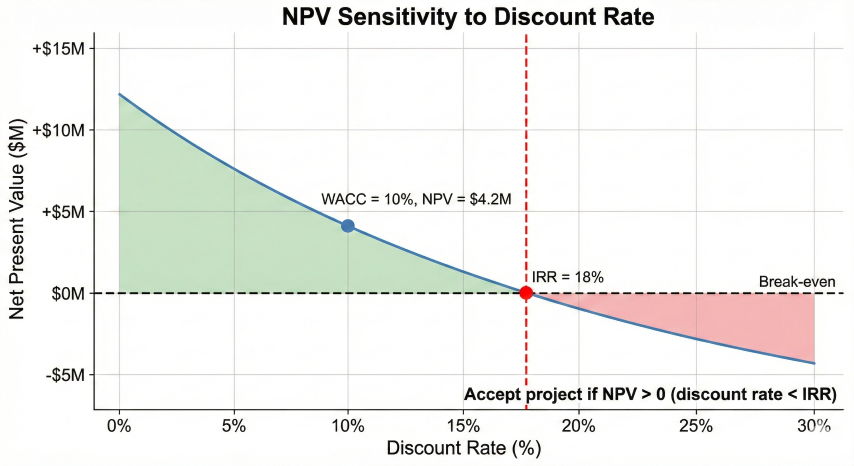

NPV profile showing how net present value decreases as discount rate increases, crossing zero at the internal rate of return (IRR = 18%).

Mid-Year Convention

For more accuracy, assume cash flows occur mid-year instead of year-end:

Mid-Year Discounting:

Standard (year-end): PV = CF / (1+r)^t

Mid-year: PV = CF / (1+r)^(t-0.5)

Effect: Increases NPV slightly (cash received sooner)

For Year 1 cash flow at 10% discount:

Year-end PV: CF / 1.10 = 0.9091 × CF

Mid-year PV: CF / 1.10^0.5 = CF / 1.0488 = 0.9535 × CF

Difference: ~4.8% higher PV with mid-year convention

Use mid-year for monthly/continuous cash flows (tariff revenue)

Use year-end for annual lump sums (tax payments)

Common NPV Pitfalls

Ignoring taxes: Use after-tax cash flows; depreciation creates tax shield

Sunk costs: Exclude past expenditures (e.g., feasibility studies already paid)

Allocated overhead: Include only incremental costs caused by project

Inflation: Match nominal cash flows with nominal discount rate, or real with real

Working capital: Include working capital investment and recovery

Opportunity cost: Include forgone alternatives (e.g., land could be sold)

Tax considerations: Pipelines use MACRS depreciation (15-year or 20-year property). Depreciation is non-cash expense that reduces taxable income, creating tax shield. Tax shield value = Depreciation × Tax Rate. Must include in cash flow analysis.

3. Discount Rate & WACC

The discount rate represents the opportunity cost of capital - the return investors could earn on alternative investments of similar risk. WACC is the most common discount rate for corporate investments.

Weighted Average Cost of Capital (WACC)

WACC Formula:

WACC = (E/V) × r_e + (D/V) × r_d × (1 - T_c)

Where:

WACC = Weighted average cost of capital

E = Market value of equity

D = Market value of debt

V = E + D = Total firm value

r_e = Cost of equity (required return on equity)

r_d = Cost of debt (interest rate on debt)

T_c = Corporate tax rate

(1 - T_c) = Tax shield on debt interest

Interpretation:

- First term: Cost of equity, weighted by equity proportion

- Second term: After-tax cost of debt, weighted by debt proportion

- Debt is tax-deductible, so after-tax cost is r_d × (1-T_c)

Cost of Equity - CAPM

Cost of equity calculated using Capital Asset Pricing Model:

Fisher Equation:

(1 + r_nominal) = (1 + r_real) × (1 + inflation)

Or approximately:

r_nominal ≈ r_real + inflation

Where:

r_nominal = Nominal discount rate (includes inflation)

r_real = Real discount rate (inflation-adjusted)

inflation = Expected inflation rate

Example: If WACC = 9% nominal and inflation = 2.5%

r_real = (1.09 / 1.025) - 1 = 6.34%

Consistency requirement:

- Nominal cash flows → use nominal discount rate

- Real cash flows → use real discount rate

Most corporate analyses use nominal rates and nominal cash flows

WACC limitations: WACC assumes constant capital structure and risk over project life. For projects that change company risk profile or financing, use APV (Adjusted Present Value) method. For very long projects (30+ years), consider declining discount rate (lower rates for distant cash flows).

4. Sensitivity Analysis

Sensitivity analysis examines how NPV changes when key assumptions vary. Essential for understanding project risk and identifying critical success factors.

One-Way Sensitivity

Vary one input at a time while holding others constant:

Example: Pipeline Lateral Sensitivity

Base case:

- Initial investment: $37M

- Annual revenue: $8M

- Annual OPEX: $2M

- Discount rate: 10%

- Project life: 20 years

- Base NPV: $14.82M

Sensitivity to revenue (±20%):

Revenue at $6.4M/yr (-20%): NPV = -$2.26M (REJECT)

Revenue at $8.0M/yr (base): NPV = $14.82M

Revenue at $9.6M/yr (+20%): NPV = $31.90M

Sensitivity to discount rate:

At 8% WACC: NPV = $21.63M

At 10% WACC (base): NPV = $14.82M

At 12% WACC: NPV = $9.17M

At 15% WACC: NPV = $0.40M (barely positive)

Critical insight: Project very sensitive to revenue; less sensitive to WACC

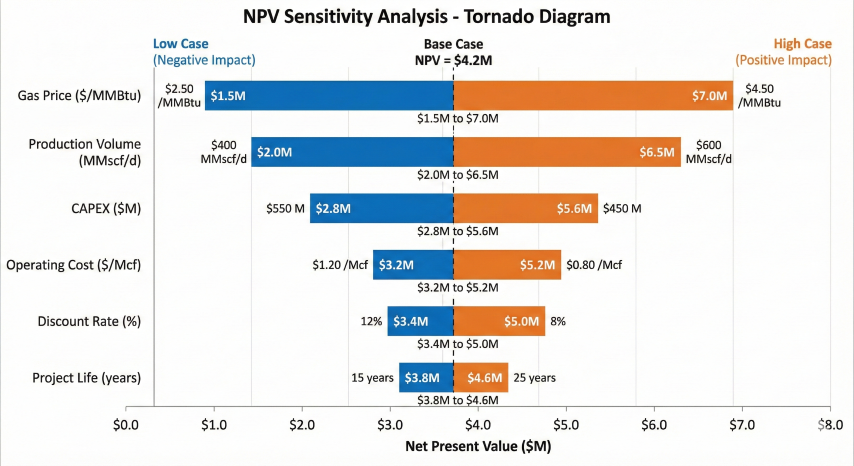

Tornado Diagram

Bar chart showing impact of each variable on NPV:

Tornado diagram ranking input variables by their impact on NPV. Gas price and production volume are the most sensitive variables requiring careful estimation.

Break-Even Revenue:

For lateral example, find revenue that gives NPV = 0:

0 = -37 + (Rev - 2) × [(1 - 1.10^-20) / 0.10] + 0.74

0 = -37 + (Rev - 2) × 8.514 + 0.74

0 = -36.26 + 8.514 × Rev - 17.03

0 = 8.514 × Rev - 53.29

Rev_breakeven = 53.29 / 8.514 = $6.26M/year

Interpretation: Need at least $6.26M annual revenue for positive NPV

Base case $8M is 27% above breakeven (good margin)

Break-even capacity (if tariff = $2/Mcf):

Q_breakeven = 6.26M / $2 = 3.13 MMcf/day

Monte Carlo Simulation

Probabilistic analysis using random sampling:

Monte Carlo NPV Simulation:

Define probability distributions for key variables:

- Revenue: Normal(μ=$8M, σ=$1.5M)

- OPEX: Normal(μ=$2M, σ=$0.4M)

- CAPEX: Triangular(min=$33M, mode=$37M, max=$42M)

- Discount rate: Fixed at 10%

Run 10,000 simulations:

1. Randomly sample revenue, OPEX, CAPEX from distributions

2. Calculate NPV for each draw

3. Compile NPV distribution

Results (example):

- Mean NPV: $14.5M

- Median NPV: $14.8M

- Std Dev: $8.2M

- P(NPV > 0): 92% (8% risk of loss)

- P(NPV > $20M): 25%

- 5th percentile NPV: -$2.1M (worst case)

- 95th percentile NPV: $29.3M (best case)

Decision: 92% probability of positive NPV supports investment

Decision Trees for Sequential Decisions

Analyze projects with decision points over time:

Example: Two-Phase Pipeline Expansion

Year 0: Decide whether to build Phase 1 ($30M)

Year 3: If demand high, build Phase 2 ($40M); if low, abandon

Phase 1 alone:

- High demand (60% prob): NPV = $20M

- Low demand (40% prob): NPV = -$5M

Phase 2 (if built in Year 3 after high demand):

- Additional NPV = $35M (discounted to Year 3)

- PV at Year 0 = 35M / (1.10)^3 = $26.3M

Decision tree:

Year 0: Build Phase 1

Year 3 (if high demand): Build Phase 2

Year 3 (if low demand): Do not build Phase 2

Expected NPV:

E(NPV) = 0.60 × (20 + 26.3) + 0.40 × (-5)

E(NPV) = 0.60 × 46.3 + 0.40 × (-5)

E(NPV) = 27.78 - 2.0 = $25.78M

Option value from flexibility: $25.78M vs. $11M (Phase 1 only expected NPV)

Real options: Projects with flexibility (expand, contract, abandon, delay) have option value beyond simple NPV. Use decision trees or real options analysis (Black-Scholes for deferral option) to capture value of managerial flexibility in uncertain environments.

5. Practical Applications

Capital Budgeting - Portfolio Selection

Allocate limited capital across competing projects:

Example: $100M Capital Budget, 5 Projects Available

Project A: Lateral extension

- CAPEX: $37M, NPV: $14.8M, IRR: 15.1%, PI: 0.40

Project B: Compressor upgrade

- CAPEX: $25M, NPV: $8.2M, IRR: 14.5%, PI: 0.33

Project C: Integrity replacement

- CAPEX: $15M, NPV: $3.5M, IRR: 11.8%, PI: 0.23

Project D: Metering system

- CAPEX: $8M, NPV: $4.1M, IRR: 18.2%, PI: 0.51

Project E: Greenfield pipeline

- CAPEX: $65M, NPV: $22.0M, IRR: 13.2%, PI: 0.34

Ranking by NPV:

1. Project E: $22.0M

2. Project A: $14.8M

3. Project B: $8.2M

4. Project D: $4.1M

5. Project C: $3.5M

Total NPV if all accepted: $52.6M

Total CAPEX required: $150M (exceeds $100M budget)

Solution 1: Rank by NPV (accept E, A, B, D)

Total CAPEX: $135M (still exceeds budget)

Solution 2: Rank by PI (value per dollar invested)

1. Project D: PI = 0.51

2. Project A: PI = 0.40

3. Project E: PI = 0.34

4. Project B: PI = 0.33

5. Project C: PI = 0.23

Accept D + A + B: CAPEX = $70M, Total NPV = $27.1M ✓

Add C: CAPEX = $85M, Total NPV = $30.6M ✓

Optimal portfolio: D, A, B, C for $85M CAPEX, $30.6M NPV

Remaining $15M for smaller projects or reserve

Best practices: Always perform sensitivity analysis on key assumptions (tariff, throughput, CAPEX). Use probability-weighted scenarios for high-uncertainty projects. Include real options value for flexible projects (phased expansion, abandonment options). Conservative assumptions better than optimistic for capital approval.

Industry Standards and References

FERC regulations: Federal Energy Regulatory Commission tariff and rate-making guidelines for interstate pipelines

IRS Publication 946: MACRS depreciation for pipeline assets (15-year or 20-year property)

SEC guidance: Proved reserves and project valuation disclosure requirements

GAAP/IFRS: Accounting standards for capital investments and impairment testing

Project Management Institute (PMI): Economic analysis standards and best practices