Evaluate midstream infrastructure investments using Net Present Value (NPV), Internal Rate of Return (IRR), and discounted cash flow (DCF) analysis per AACE International and SPE guidelines.

Calculate NPV, IRR, MIRR, and PI for pipeline projects

Determine appropriate discount rates (WACC)

Perform sensitivity, scenario, and decision-tree analysis

Evaluate depreciation tax shields (MACRS)

Apply NPV to capital budgeting, replacement, tariff, and acquisition decisions

1. NPV Fundamentals

Net Present Value (NPV) is the gold standard for capital budgeting decisions. It measures the absolute dollar value a project adds to shareholder wealth by discounting all future cash flows to present value and subtracting the initial investment.

NPV Definition

Sum of discounted cash flows

Present value of all future cash flows minus initial investment.

Decision Rule

NPV > 0: Accept

Positive NPV means project creates shareholder value.

Key Advantage

Measures absolute value

Unlike IRR, NPV shows actual dollars of wealth created.

Discount Rate

WACC or hurdle rate

Use company's weighted average cost of capital.

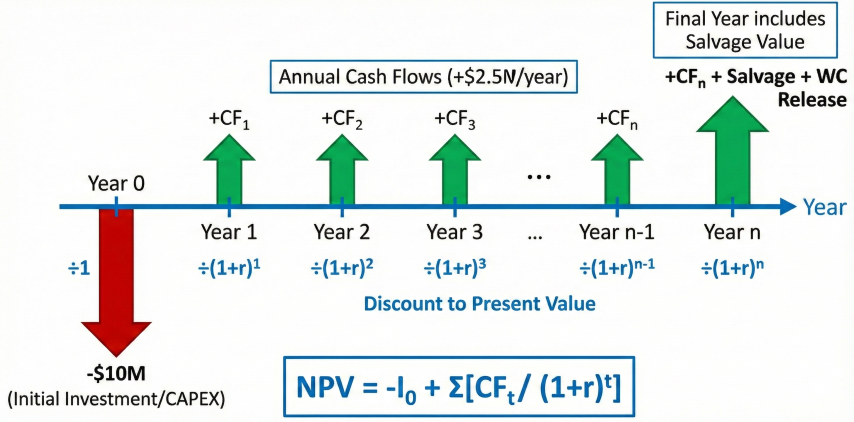

NPV Formula

Net Present Value:

NPV = -I₀ + CF₁/(1+r)¹ + CF₂/(1+r)² + ... + CFₙ/(1+r)ⁿ

Or in summation notation:

NPV = Σ [CFₜ / (1 + r)ᵗ] for t = 0 to n

Where:

I₀ = Initial investment at t=0 ($)

CFₜ = Cash flow in period t ($)

r = Discount rate (WACC, decimal)

n = Project life (years)

NPV Cash Flow Timeline: Initial investment at Year 0, annual cash flows discounted to present value, with terminal value including salvage and working capital release.

IRR ignores scale; $50M project with 12% IRR may beat $5M project with 20% IRR

Non-conventional cash flows

Yes

No

Multiple sign changes create multiple IRRs

Single project go/no-go

Yes

Yes

Both give same accept/reject decision

Management communication

No

Yes

IRR as % is easier to communicate than NPV in $

NPV Rule: When NPV and IRR rank projects differently, always use NPV. NPV assumes cash flows are reinvested at WACC (realistic), while IRR assumes reinvestment at IRR itself (often unrealistic for high-IRR projects).

NPV Decision Framework

NPV Result

Meaning

Decision

NPV > 0

Project returns exceed cost of capital

Accept - creates shareholder value

NPV = 0

Project returns equal cost of capital

Indifferent - no value creation/destruction

NPV < 0

Project returns below cost of capital

Reject - destroys shareholder value

NPV₁ > NPV₂

Mutually exclusive projects

Select Project 1 (higher NPV)

Why NPV is preferred: NPV directly measures dollar value created, accounts for all cash flows, incorporates time value of money, and uses realistic discount rate (WACC). Superior to payback period or accounting rate of return for capital budgeting decisions.

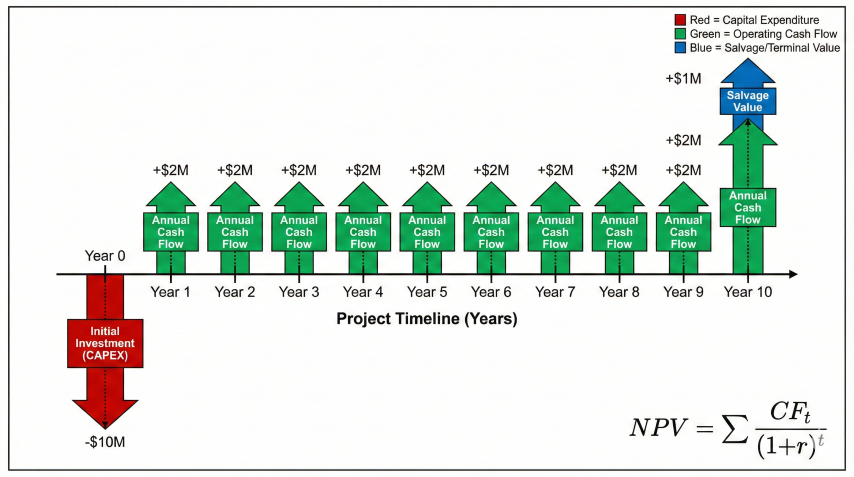

Types of Cash Flows

Project cash flow timeline illustrating initial investment, annual operating cash flows, and terminal salvage value used in NPV calculations.

Terminal cash flow (Year N): Salvage value, working capital recovery, decommissioning costs

Tax effects: Depreciation tax shield, capital gains/losses on disposal

Common Pipeline Investment Types

Project Type

Typical Investment

Cash Flow Profile

Project Life

Greenfield transmission pipeline

$500M - $5B

Large upfront CAPEX, stable long-term revenue

30-50 years

Lateral extension

$10M - $100M

Moderate CAPEX, incremental revenue

20-30 years

Compressor station upgrade

$20M - $200M

CAPEX, reduced fuel costs, increased capacity

15-25 years

Integrity/replacement

$5M - $50M

CAPEX, avoided failure costs, maintained revenue

10-20 years

Metering/automation

$1M - $10M

CAPEX, reduced labor, improved accuracy

10-15 years

Discount Factor Reference Values

Present Value Factor:

PV Factor = 1 / (1 + r)^t

This is the present value of $1 received in year t.

Example discount factors at r = 10%:

Year 1: PV = 1/1.10 = 0.9091 (each dollar worth $0.91 today)

Year 5: PV = 1/(1.10)^5 = 0.6209

Year 10: PV = 1/(1.10)^10 = 0.3855

Year 20: PV = 1/(1.10)^20 = 0.1486

Note: Distant cash flows heavily discounted (Year 20 dollar worth only $0.15 today)

Worked Example: 20-Mile Pipeline Lateral (Annuity Approach)

Example: 20-Mile Lateral Extension

Initial investment (Year 0):

- Pipeline construction: $25M

- Compressor station: $10M

- Land and permits: $2M

Total CAPEX: I₀ = -$37M

Annual cash flows (Years 1-20):

- Revenue (tariff): $8M/year

- Operating expenses: -$2M/year

- Net annual cash flow: CF = $6M/year

Discount rate: r = 10% (WACC)

Salvage value (Year 20): S = $5M

NPV Calculation:

Method 1: Year-by-year

NPV = -37 + 6/(1.10)¹ + 6/(1.10)² + ... + 6/(1.10)²⁰ + 5/(1.10)²⁰

Method 2: Annuity formula (equal cash flows)

PV of annuity = CF × [(1 - (1+r)^-N) / r]

PV of annuity = 6 × [(1 - 1.10^-20) / 0.10]

PV of annuity = 6 × [0.8514 / 0.10]

PV of annuity = 6 × 8.514 = $51.08M

PV of salvage = 5 / (1.10)^20 = 5 × 0.1486 = $0.74M

NPV = -37 + 51.08 + 0.74 = $14.82M

IRR Calculation (find r where NPV = 0):

By iteration (Excel IRR function): IRR = 15.4%

Since IRR (15.4%) > WACC (10%), project exceeds cost of capital by 5.4 pp.

Decision: Accept project (NPV > 0, creates $14.82M value, IRR > WACC)

Profitability Index

Profitability Index (PI):

PI = PV(Cash Inflows) / PV(Cash Outflows) = 1 + NPV / Initial Investment

For the 20-mile lateral example above:

PI = 1 + 14.82 / 37 = 1.40

Interpretation: PV of inflows is 1.40× the initial investment;

each $1 invested returns $1.40 of present value (i.e., $0.40 of NPV).

Decision rule:

PI > 1: Accept (equivalent to NPV > 0)

PI < 1: Reject

Use for capital rationing: Rank projects by PI when budget limited.

PI is especially useful when comparing projects of different sizes

within a fixed capital budget.

Unequal Cash Flows Example

Many midstream projects have varying cash flows over time as tariffs escalate, volumes ramp, or contracts step up:

Example: Compressor Station with Increasing Tariffs

Year 0: CAPEX = -$50M

Year 1-5: CF = $8M/year

Year 6-10: CF = $10M/year (tariff increase)

Year 11-15: CF = $12M/year

Year 15: Salvage = $8M

Discount rate: r = 9%

Calculate NPV by summing discounted cash flows by tranche:

Years 1-5: PV = 8 × [(1-1.09^-5)/0.09] = 8 × 3.8897 = $31.12M

Years 6-10: PV = 10 × [(1-1.09^-5)/0.09] × (1.09)^-5 = 10 × 3.8897 × 0.6499 = $25.28M

Years 11-15: PV = 12 × [(1-1.09^-5)/0.09] × (1.09)^-10 = 12 × 3.8897 × 0.4224 = $19.72M

Salvage: PV = 8 / (1.09)^15 = 8 × 0.2745 = $2.20M

NPV = -50 + 31.12 + 25.28 + 19.72 + 2.20 = $28.32M ✓

Project highly attractive with NPV = $28M

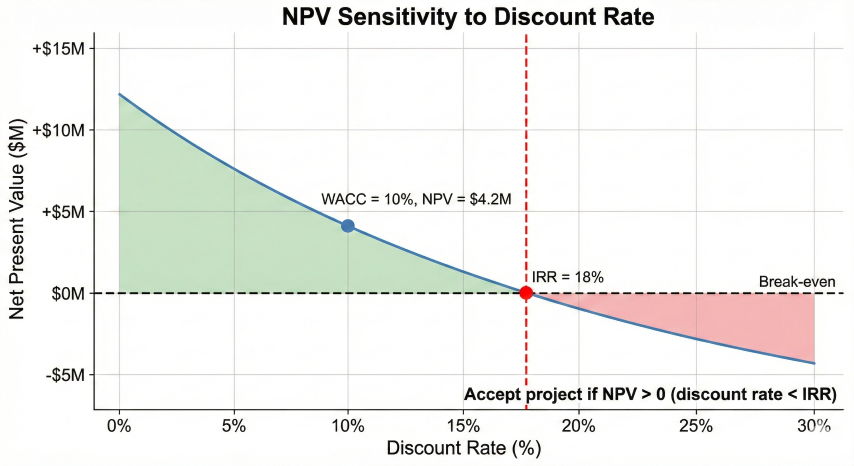

NPV profile showing how net present value decreases as discount rate increases, crossing zero at the internal rate of return (IRR = 18%).

Mid-Year Convention

For more accuracy, assume cash flows occur mid-year instead of year-end:

Mid-Year Discounting:

Standard (year-end): PV = CF / (1+r)^t

Mid-year: PV = CF / (1+r)^(t-0.5)

Effect: Increases NPV slightly (cash received sooner)

For Year 1 cash flow at 10% discount:

Year-end PV: CF / 1.10 = 0.9091 × CF

Mid-year PV: CF / 1.10^0.5 = CF / 1.0488 = 0.9535 × CF

Difference: ~4.8% higher PV with mid-year convention

Use mid-year for monthly/continuous cash flows (tariff revenue)

Use year-end for annual lump sums (tax payments)

Common NPV Pitfalls

Ignoring taxes: Use after-tax cash flows; depreciation creates tax shield

Sunk costs: Exclude past expenditures (e.g., feasibility studies already paid)

Allocated overhead: Include only incremental costs caused by project

Inflation: Match nominal cash flows with nominal discount rate, or real with real

Working capital: Include working capital investment and recovery

Opportunity cost: Include forgone alternatives (e.g., land could be sold)

Tax considerations: Pipelines use MACRS depreciation (15-year or 20-year property). Depreciation is non-cash expense that reduces taxable income, creating tax shield. Tax shield value = Depreciation × Tax Rate. Must include in cash flow analysis (see Section 4).

2. IRR & MIRR Methods

Internal Rate of Return (IRR) is the discount rate that makes NPV equal to zero. It represents the project's effective annual return. However, IRR has limitations that Modified IRR (MIRR) addresses.

IRR Formula

IRR Definition:

Find r such that NPV = 0:

0 = -I₀ + CF₁/(1+IRR)¹ + CF₂/(1+IRR)² + ... + CFₙ/(1+IRR)ⁿ

Decision Rules:

- IRR > WACC → Accept project

- IRR < WACC → Reject project

- IRR = WACC → Indifferent (NPV = 0)

IRR cannot be solved algebraically for n > 2.

Use Newton-Raphson iteration or financial calculator.

NPV Profile Chart: NPV decreases with higher discount rates. IRR occurs where curve crosses zero. Accept projects when discount rate < IRR (NPV > 0).

MIRR solves two IRR problems: (1) unrealistic reinvestment assumption and (2) multiple IRRs with non-conventional cash flows.

MIRR Formula:

MIRR = [(FV of positive CFs / |PV of negative CFs|)^(1/n)] - 1

Where:

- Positive CFs compounded forward at reinvestment rate (typically WACC)

- Negative CFs discounted back at finance rate (cost of debt or WACC)

FV = Σ [CFₜ × (1 + r_reinvest)^(n-t)] for CFₜ > 0

PV = Σ [|CFₜ| / (1 + r_finance)^t] for CFₜ < 0

MIRR is always unique (single solution).

MIRR < IRR when IRR > reinvestment rate (typical case).

Example: IRR vs MIRR Comparison

Pipeline Project:

Cash flows: CF₀ = -$10M, CF₁...₈ = $2.5M/year

WACC = 10%

IRR Calculation:

By iteration: IRR = 18.6%

MIRR Calculation (reinvest at 10%):

FV of positive CFs = $2.5M × [(1.10)⁷ + (1.10)⁶ + ... + 1.0]

FV = $2.5M × 11.436 = $28.59M

PV of negative CF = $10M (at t=0)

MIRR = ($28.59M / $10M)^(1/8) - 1

MIRR = (2.859)^0.125 - 1

MIRR = 14.0%

MIRR (14.0%) < IRR (18.6%)

MIRR is more realistic because it assumes reinvestment at WACC (10%), not at IRR (18.6%).

Multiple IRR Problem

Cash Flow Pattern

IRR Count

Example

Solution

Conventional (-, +, +, +)

1 unique

Standard pipeline project

Use IRR normally

Non-conventional (-, +, +, -)

0, 1, or 2+

Mining with reclamation cost

Use NPV or MIRR

All negative

None

Pure cost project

Use cost-benefit analysis

Best Practice: Many midstream companies now require both IRR and MIRR for capital approval. MIRR provides a more conservative, realistic return estimate. Use MIRR when comparing projects with different cash flow timing patterns.

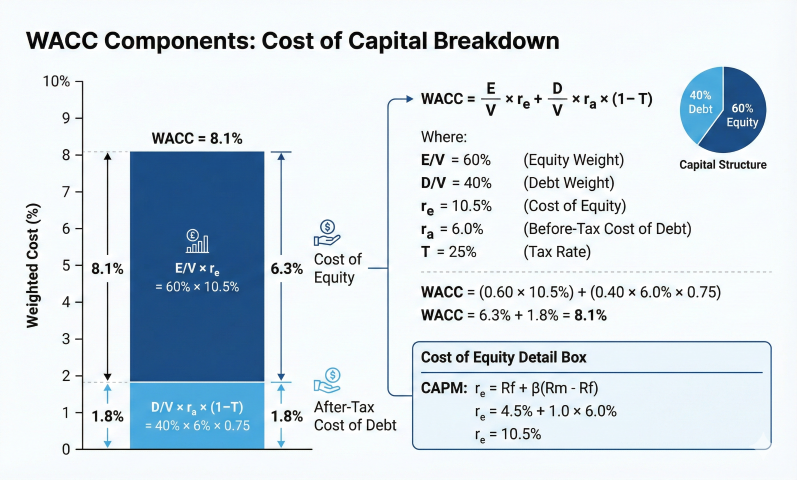

3. WACC & Discount Rates

The Weighted Average Cost of Capital (WACC) represents the blended cost of all capital sources. It is the appropriate discount rate for projects of average risk. Project-specific risk adjustments may be added.

WACC Formula

Weighted Average Cost of Capital:

WACC = (E/V) × rₑ + (D/V) × r_d × (1 - T_c)

Where:

E = Market value of equity ($)

D = Market value of debt ($)

V = E + D = Total firm value ($)

rₑ = Cost of equity (%)

r_d = Cost of debt, before tax (%)

T_c = Corporate tax rate (%)

(1 - T_c) = Tax shield on interest

Target capital structure:

E/V = Equity weight (typically 50-70% for midstream)

D/V = Debt weight (typically 30-50% for midstream)

WACC Components: Weighted average of cost of equity (via CAPM) and after-tax cost of debt, reflecting target capital structure.

Discount Rate Sensitivity: A 2% change in WACC can swing NPV by 20-30% for long-lived infrastructure. For a 20-year project with $100M investment and $15M/year cash flows: NPV at 8% = $47M, NPV at 10% = $28M (40% lower). Always test sensitivity to discount rate assumptions.

Typical WACC by Industry Segment

Industry Segment

Typical WACC

Risk Characteristics

Regulated pipelines (interstate)

7-9%

Low risk, stable tariffs, regulatory protection

Gathering & processing

9-11%

Moderate risk, commodity price exposure

Midstream MLPs

8-10%

Fee-based, long-term contracts

Export terminals (LNG)

10-12%

Higher risk, international exposure, large CAPEX

E&P (upstream)

12-15%

High risk, commodity price volatility

Real vs. Nominal Rates (Fisher Equation)

Fisher Equation:

(1 + r_nominal) = (1 + r_real) × (1 + inflation)

Or approximately:

r_nominal ≈ r_real + inflation

Where:

r_nominal = Nominal discount rate (includes inflation)

r_real = Real discount rate (inflation-adjusted)

inflation = Expected inflation rate

Example: If WACC = 9% nominal and inflation = 2.5%

r_real = (1.09 / 1.025) - 1 = 6.34%

Consistency requirement:

- Nominal cash flows → use nominal discount rate

- Real cash flows → use real discount rate

Most corporate analyses use nominal rates and nominal cash flows.

WACC limitations: WACC assumes constant capital structure and risk over project life. For projects that change company risk profile or financing, use APV (Adjusted Present Value) method. For very long projects (30+ years), consider declining discount rate (lower rates for distant cash flows).

4. Cash Flow Analysis

Accurate cash flow forecasting is the foundation of reliable NPV/IRR analysis. Free Cash Flow to Firm (FCFF) is the appropriate measure for project evaluation.

Free Cash Flow Formula

Free Cash Flow to Firm (FCFF):

FCFF = EBIT × (1 - Tax) + Depreciation - CAPEX - ΔWC

Or equivalently:

FCFF = Revenue - OPEX - Taxes + Depreciation × Tax - CAPEX - ΔWC

Where:

EBIT = Earnings before interest and taxes

Tax = Marginal corporate tax rate (21% federal + state)

Depreciation = Non-cash charge (creates tax shield)

CAPEX = Capital expenditures

ΔWC = Change in working capital (increase = outflow)

Note: Interest is NOT subtracted from FCFF.

WACC already accounts for financing costs.

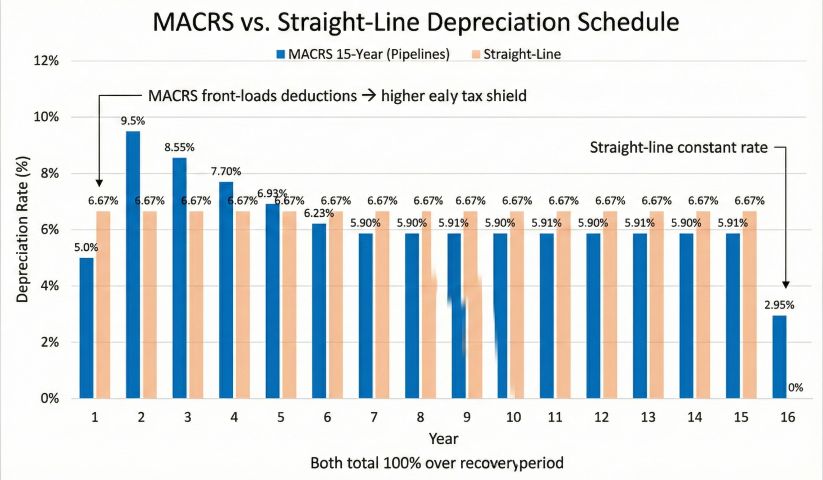

Depreciation Tax Shield

Depreciation reduces taxable income, creating a "tax shield" that increases after-tax cash flow. Accelerated depreciation (MACRS) provides higher tax shields in early years, increasing NPV.

MACRS vs. Straight-Line Depreciation: MACRS front-loads deductions, providing higher tax shields in early years and increasing NPV compared to straight-line depreciation.

MACRS 15-Year Schedule (Pipelines)

Year

Rate

Year

Rate

1

5.00%

9

5.91%

2

9.50%

10

5.90%

3

8.55%

11

5.91%

4

7.70%

12

5.90%

5

6.93%

13

5.91%

6

6.23%

14

5.90%

7

5.90%

15

5.91%

8

5.90%

16

2.95%

Working Capital

Working Capital Treatment:

Working Capital (WC) = Current Assets - Current Liabilities

= Inventory + Receivables - Payables

Year 0: WC investment = cash outflow

Years 1-n: ΔWC = additional outflow if revenue grows

Final Year: WC release = cash inflow (recovered at project end)

Midstream WC Requirement: Typically 5-10% of annual revenue

- Limited inventory (gas flows through)

- Short collection cycles (monthly billing)

- Long payment terms with suppliers

Terminal Value

Terminal Value Methods:

1. Salvage Value (asset-based):

TV = Estimated market value at end of analysis

Typical for pipelines: 20-40% of original cost

Tax on gain: (Salvage - Book Value) × Tax Rate

2. Perpetuity Growth Model:

TV = FCF(final) × (1 + g) / (WACC - g)

g = perpetual growth rate (typically 0-2%)

3. Exit Multiple:

TV = EBITDA(final) × EV/EBITDA multiple

Midstream multiples: 8-12× EBITDA

Terminal value often represents 30-50% of total NPV

for long-lived infrastructure projects.

Cash Flow Accuracy: NPV is most sensitive to near-term cash flows due to discounting. A 10% error in Year 5 cash flow has 10× more impact than a 10% error in Year 25. Focus forecasting effort on Years 1-10; far-future cash flows can use simplified assumptions.

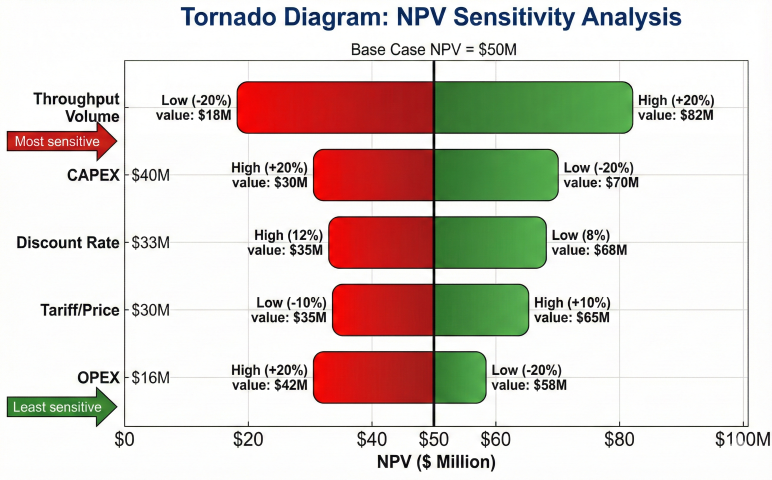

5. Sensitivity & Risk Analysis

Sensitivity analysis tests how NPV/IRR change with key input variables. For midstream projects, the primary sensitivities are typically throughput volume, commodity prices (for processing plants), CAPEX, and discount rate.

One-Way Sensitivity (Tornado Chart)

Sensitivity Analysis Process:

1. Identify key variables (typically 5-8 drivers)

2. Define range: ±10%, ±20%, or min/max bounds

3. Vary one variable, hold others at base case

4. Calculate NPV at each scenario

5. Rank by impact (tornado diagram)

Example Results ($100M pipeline, base NPV = $50M):

Variable | -10% | Base | +10% | Swing

------------------|---------|--------|--------|-------

Throughput volume | $18M | $50M | $82M | $64M

Discount rate | $68M | $50M | $35M | $33M

CAPEX | $60M | $50M | $40M | $20M

OPEX | $56M | $50M | $44M | $12M

Ranking: Volume > Discount Rate > CAPEX > OPEX

Tornado Sensitivity Diagram: Variables ranked by NPV impact. Throughput volume is the primary driver; OPEX has minimal effect. Red/green bars show NPV range from low to high scenarios.

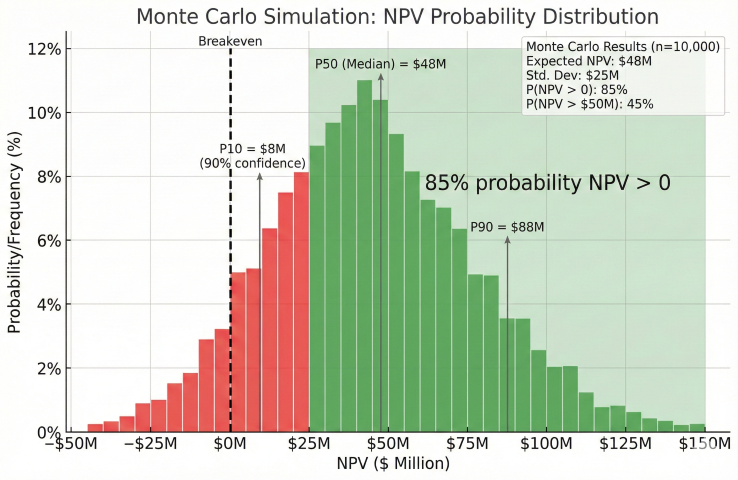

Probabilistic Analysis:

Define probability distributions for uncertain variables:

- Volume: Log-normal (mean 200, std dev 30 MMcf/d)

- CAPEX: Triangular (min $90M, mode $100M, max $120M)

- Tariff: Uniform ($0.45 to $0.55/Mcf)

Run 10,000+ iterations:

- Sample each variable from its distribution

- Calculate NPV for each iteration

- Build probability distribution of outcomes

Results:

- Expected NPV (mean): $48M

- Standard deviation: $25M

- P(NPV > 0): 85%

- P(NPV > $50M): 45%

- VaR (P10): NPV > $8M with 90% confidence

Decision: 85% probability of positive NPV is acceptable

for most corporate risk tolerances (>70% threshold).

Monte Carlo NPV Distribution: Probabilistic analysis from 10,000 simulations shows 85% probability of NPV > 0. P10/P50/P90 values quantify uncertainty range.

Industry Practice: Most midstream companies require projects to show positive NPV in both base case and pessimistic (P90) scenarios before approval. The "sanction hurdle" is typically IRR > WACC + 2-3% to provide buffer for execution risk and model uncertainty.

Worked Sensitivity Example: Pipeline Lateral

Example: 20-Mile Lateral Sensitivity

Base case (from Section 1 example):

- Initial investment: $37M

- Annual revenue: $8M

- Annual OPEX: $2M

- Discount rate: 10%

- Project life: 20 years

- Base NPV: $14.82M

Sensitivity to revenue (±20%):

Revenue at $6.4M/yr (-20%): NPV = +$1.20M (ACCEPT)

Revenue at $8.0M/yr (base): NPV = $14.82M

Revenue at $9.6M/yr (+20%): NPV = $28.44M

Sensitivity to discount rate:

At 8% WACC: NPV = $21.63M

At 10% WACC (base): NPV = $14.82M

At 12% WACC: NPV = $9.17M

At 15% WACC: NPV = $0.40M (barely positive)

Critical insight: Project very sensitive to revenue; less sensitive to WACC

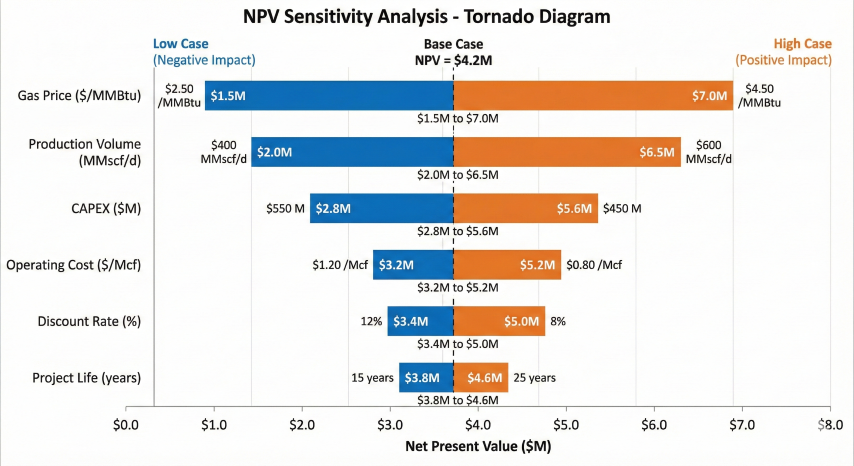

Tornado diagram ranking input variables by their impact on NPV. Gas price and production volume are the most sensitive variables requiring careful estimation.

Example: Two-Phase Pipeline Expansion

Year 0: Decide whether to build Phase 1 ($30M)

Year 3: If demand high, build Phase 2 ($40M); if low, abandon

Phase 1 alone:

- High demand (60% prob): NPV = $20M

- Low demand (40% prob): NPV = -$5M

Phase 2 (if built in Year 3 after high demand):

- Additional NPV = $35M (discounted to Year 3)

- PV at Year 0 = 35M / (1.10)^3 = $26.3M

Decision tree:

Year 0: Build Phase 1

Year 3 (if high demand): Build Phase 2

Year 3 (if low demand): Do not build Phase 2

Expected NPV:

E(NPV) = 0.60 × (20 + 26.3) + 0.40 × (-5)

E(NPV) = 0.60 × 46.3 + 0.40 × (-5)

E(NPV) = 27.78 - 2.0 = $25.78M

Option value from flexibility: $25.78M vs. $11M (Phase 1 only expected NPV)

Real options: Projects with flexibility (expand, contract, abandon, delay) have option value beyond simple NPV. Use decision trees or real options analysis (Black-Scholes for deferral option) to capture value of managerial flexibility in uncertain environments.

6. Practical Applications

Capital Budgeting — Portfolio Selection

Allocate limited capital across competing projects:

Example: $100M Capital Budget, 5 Projects Available

Project A: Lateral extension

- CAPEX: $37M, NPV: $14.8M, IRR: 15.1%, PI: 0.40

Project B: Compressor upgrade

- CAPEX: $25M, NPV: $8.2M, IRR: 14.5%, PI: 0.33

Project C: Integrity replacement

- CAPEX: $15M, NPV: $3.5M, IRR: 11.8%, PI: 0.23

Project D: Metering system

- CAPEX: $8M, NPV: $4.1M, IRR: 18.2%, PI: 0.51

Project E: Greenfield pipeline

- CAPEX: $65M, NPV: $22.0M, IRR: 13.2%, PI: 0.34

Ranking by NPV:

1. Project E: $22.0M

2. Project A: $14.8M

3. Project B: $8.2M

4. Project D: $4.1M

5. Project C: $3.5M

Total NPV if all accepted: $52.6M

Total CAPEX required: $150M (exceeds $100M budget)

Solution 1: Rank by NPV (accept E, A, B, D)

Total CAPEX: $135M (still exceeds budget)

Solution 2: Rank by PI (value per dollar invested)

1. Project D: PI = 0.51

2. Project A: PI = 0.40

3. Project E: PI = 0.34

4. Project B: PI = 0.33

5. Project C: PI = 0.23

Accept D + A + B: CAPEX = $70M, Total NPV = $27.1M ✓

Add C: CAPEX = $85M, Total NPV = $30.6M ✓

Optimal portfolio: D, A, B, C for $85M CAPEX, $30.6M NPV

Remaining $15M for smaller projects or reserve

Best practices: Always perform sensitivity analysis on key assumptions (tariff, throughput, CAPEX). Use probability-weighted scenarios for high-uncertainty projects. Include real options value for flexible projects (phased expansion, abandonment options). Conservative assumptions better than optimistic for capital approval.

Industry Standards and References

FERC regulations: Federal Energy Regulatory Commission tariff and rate-making guidelines for interstate pipelines

IRS Publication 946: MACRS depreciation for pipeline assets (15-year or 20-year property)

SEC guidance: Proved reserves and project valuation disclosure requirements

GAAP/IFRS: Accounting standards for capital investments and impairment testing

Project Management Institute (PMI): Economic analysis standards and best practices

AACE International: Recommended practices for capital cost estimation and economic evaluation

SPE (Society of Petroleum Engineers): Project economics standards including SPE 84218 (Newendorp Monte Carlo methods)

7. Payback Period Analysis

Payback period is the time required for cumulative cash inflows from a project to equal the initial investment. It is one of the most widely used screening tools in capital budgeting for pipeline and midstream projects. Used alongside NPV and IRR, payback metrics provide complementary insight into liquidity recovery and risk exposure.

Pipeline expansions

Capacity additions

New compressor stations, looping, diameter increases justified by throughput revenue.

Efficiency projects

Energy savings

VFDs, insulation upgrades, heat recovery systems with utility cost reduction.

Reliability improvements

Maintenance reduction

Equipment upgrades that reduce downtime and maintenance costs.

Safety & compliance

Risk mitigation

Integrity management, leak detection, safety systems justified by avoided costs.

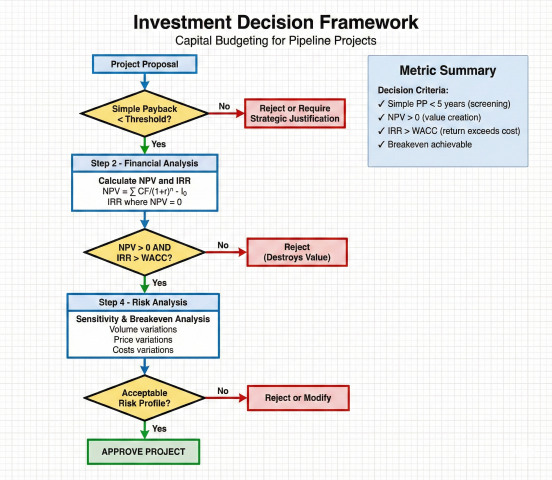

Why payback analysis matters: Simple payback provides quick go/no-go screening. Discounted payback accounts for time value of money. Combined with NPV and IRR, these metrics form a comprehensive investment decision framework.

Investment decision framework integrating payback period screening with NPV, IRR, and risk analysis for capital project evaluation

Advantages and Limitations of the Payback Method

Advantages:

Simplicity: Easy to calculate and explain to non-financial stakeholders

Risk indicator: Shorter payback means faster capital recovery and lower risk

Liquidity focus: Emphasizes cash recovery important for capital-constrained companies

Screening tool: Quick filter for obviously poor projects before detailed analysis

Limitations:

Ignores cash flows beyond payback: Doesn't consider project life or total profitability

No time value (simple): Simple payback doesn't discount future cash flows

Arbitrary cutoff: Payback threshold (e.g., 3 years) may not align with value creation

Biased against long-term projects: May reject valuable long-lived infrastructure

When cash flows vary by year, calculate cumulative cash flow and find when it equals initial investment:

Cumulative Cash Flow Method:

Cumulative CF_n = Σ(CF₁ + CF₂ + ... + CF_n)

Find n where Cumulative CF_n ≥ I₀

If recovery occurs partway through year n:

PP = (n-1) + (I₀ - Cumulative CF_(n-1)) / CF_n

Example with varying cash flows:

Initial investment: $800,000

Year 1: $150,000 → Cumulative: $150,000

Year 2: $200,000 → Cumulative: $350,000

Year 3: $250,000 → Cumulative: $600,000

Year 4: $300,000 → Cumulative: $900,000

Recovery occurs in Year 4:

Remaining after Year 3: $800,000 - $600,000 = $200,000

Fraction of Year 4: $200,000 / $300,000 = 0.67

Payback Period = 3 + 0.67 = 3.67 years

Typical Payback Thresholds by Industry

Project Type

Typical Threshold

Rationale

Energy efficiency (motors, VFDs)

2-3 years

Technology obsolescence, short economic life

Process improvements

3-5 years

Moderate risk, proven technology

Pipeline capacity expansion

4-7 years

Long-term contracts, regulated returns

New facilities (greenfield)

5-10 years

30+ year design life, strategic infrastructure

Safety/environmental compliance

Not applicable

Mandatory; justify via risk reduction, not payback

R&D / pilot projects

N/A or 1-2 years

High uncertainty; very short payback or strategic value

Pipeline Expansion Payback Example

A pipeline operator considers adding a compressor station to increase throughput from 500 MMcf/d to 650 MMcf/d.

Project Data:

Compressor station cost: $12,000,000

Additional throughput: 150 MMcf/d

Transportation tariff: $0.50/Mcf

Operating days: 350 days/year

Annual O&M cost: $1,200,000/year

Annual Revenue Increase:

Volume = 150,000 Mcf/day × 350 days = 52,500,000 Mcf/year

Revenue = 52,500,000 × $0.50 = $26,250,000/year

Net Annual Cash Flow:

CF = $26,250,000 - $1,200,000 = $25,050,000/year

Simple Payback:

PP = $12,000,000 / $25,050,000 = 0.48 years = 5.8 months

Interpretation: Very attractive project with sub-1-year payback, assuming capacity can be sold.

Energy Efficiency Payback Example (VFD Retrofit)

Replace existing fixed-speed compressor motor with VFD to reduce power consumption:

Project Data:

VFD installed cost: $85,000

Current power consumption: 400 kW average

Expected reduction: 15%

Power cost: $0.10/kWh

Operating hours: 8,000 hr/year

Annual Energy Savings:

kWh saved = 400 kW × 0.15 × 8,000 hr = 480,000 kWh/year

Cost savings = 480,000 × $0.10 = $48,000/year

Simple Payback:

PP = $85,000 / $48,000 = 1.77 years

Interpretation: Acceptable payback for energy efficiency. Project likely approved.

Rule of thumb: For midstream operators, simple payback < 3 years is considered excellent, 3-5 years is good, 5-7 years is marginal. Projects > 7 years require strategic justification beyond financial return.

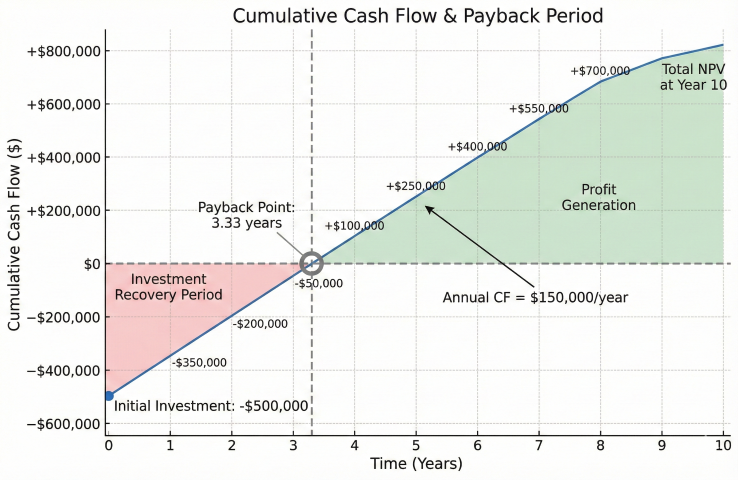

Cumulative cash flow curve illustrating payback period where cumulative returns equal initial investment

Discounted Payback Period

Discounted payback period accounts for the time value of money by discounting future cash flows to present value. This provides a more conservative and financially rigorous assessment than simple payback.

Present Value Formula:

PV = CF / (1 + r)ⁿ

Where:

PV = Present value of cash flow ($)

CF = Future cash flow in year n ($)

r = Discount rate (decimal)

n = Year number

Cumulative Present Value:

Cumulative PV_n = Σ [CF_i / (1 + r)ⁱ] for i = 1 to n

Find n where Cumulative PV_n ≥ I₀

Interpolation:

DPP = (n-1) + [(I₀ - Cumulative PV_(n-1)) / PV_n]

Where DPP = Discounted payback period (years)

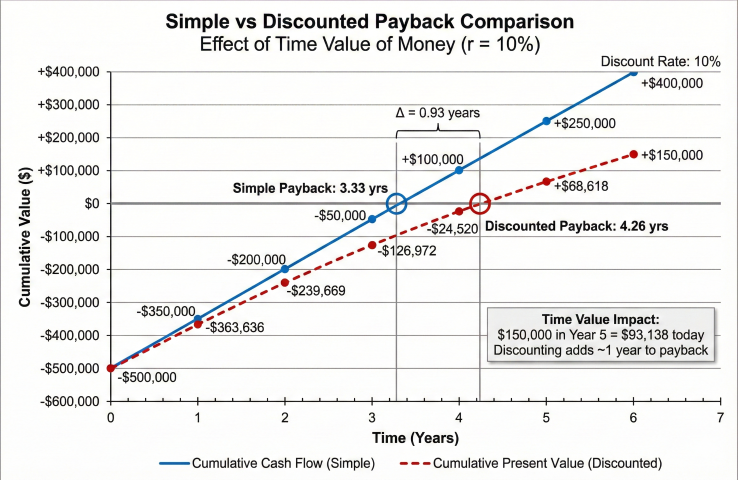

Comparison: Simple vs Discounted Payback

Project with $500,000 initial investment, 10% discount rate:

Year

Cash Flow

Cumulative CF (Simple)

PV Factor (1+0.10)ⁿ

Present Value

Cumulative PV (Discounted)

0

-$500,000

-$500,000

1.000

-$500,000

-$500,000

1

$150,000

-$350,000

1.100

$136,364

-$363,636

2

$150,000

-$200,000

1.210

$123,967

-$239,669

3

$150,000

-$50,000

1.331

$112,697

-$126,972

4

$150,000

$100,000

1.464

$102,452

-$24,520

5

$150,000

$250,000

1.611

$93,138

$68,618

Simple Payback Calculation:

Recovery in Year 4: 3 + ($50,000 / $150,000) = 3.33 years

Discounted Payback Calculation:

Recovery in Year 5: 4 + ($24,520 / $93,138) = 4.26 years

Difference: 4.26 - 3.33 = 0.93 years longer

Interpretation: Discounting increases payback by ~1 year due to time value of money.

The $150,000 received in Year 5 is worth only $93,138 today.

Selecting the Discount Rate for Payback

Discount Rate Type

Typical Range

When to Use

WACC (Weighted Average Cost of Capital)

8-12%

Standard projects with average risk profile

Hurdle rate (WACC + risk premium)

12-18%

High-risk projects, new technologies, uncertain markets

Alternative WACC Calculation Example (60/40 Capital Structure with Different Numbers)

Weighted Average Cost of Capital — Alternative Example:

WACC = (E/V) × Re + (D/V) × Rd × (1 - Tc)

Equity: $100M at 12% cost

Debt: $40M at 6% cost

Tax rate: 25%

E/V = $100M / $140M = 71.4%

D/V = $40M / $140M = 28.6%

WACC = 0.714 × 12% + 0.286 × 6% × (1 - 0.25)

WACC = 8.57% + 1.29% = 9.86% ≈ 10%

Impact of discount rate on payback: Higher discount rates penalize distant cash flows more heavily, increasing discounted payback period. A 5% increase in discount rate typically adds 0.5-1.5 years to payback for 5-10 year projects.

Simple vs discounted payback comparison showing how time value of money extends payback period by approximately one year at 10% discount rate

When Projects Never Pay Back

Some projects have negative NPV and never achieve discounted payback:

Example of No Payback:

Initial investment: $1,000,000

Annual cash flow: $80,000/year for 20 years

Discount rate: 12%

PV of cash flows = $80,000 × [PV annuity factor, 12%, 20 years]

PV = $80,000 × 7.469 = $597,520

Since $597,520 < $1,000,000, project never pays back in PV terms.

NPV = -$1,000,000 + $597,520 = -$402,480 (reject project)

Payback-Based Breakeven Throughput

For capacity expansion projects, calculate minimum volume needed to recover investment within a target payback:

Breakeven Volume Calculation:

Total Annual Cost = (I₀ / PP) + Annual O&M

Required Volume = Total Annual Cost / Unit Margin

Where:

I₀ = Initial investment

PP = Target payback period (years)

Unit Margin = Tariff revenue per unit - variable cost per unit

Example - Pipeline Looping:

Investment: $25,000,000

Target payback: 5 years

Annual O&M: $800,000/year

Tariff: $0.75/Mcf

Variable cost: $0.05/Mcf

Annual cost to recover = $25,000,000 / 5 + $800,000 = $5,800,000

Unit margin = $0.75 - $0.05 = $0.70/Mcf

Breakeven volume = $5,800,000 / $0.70 = 8,285,714 Mcf/year

= 22,710 Mcf/day (assuming 365 days)

If project adds 200 MMcf/d capacity and can sell 25 MMcf/d or more,

project exceeds breakeven requirement.

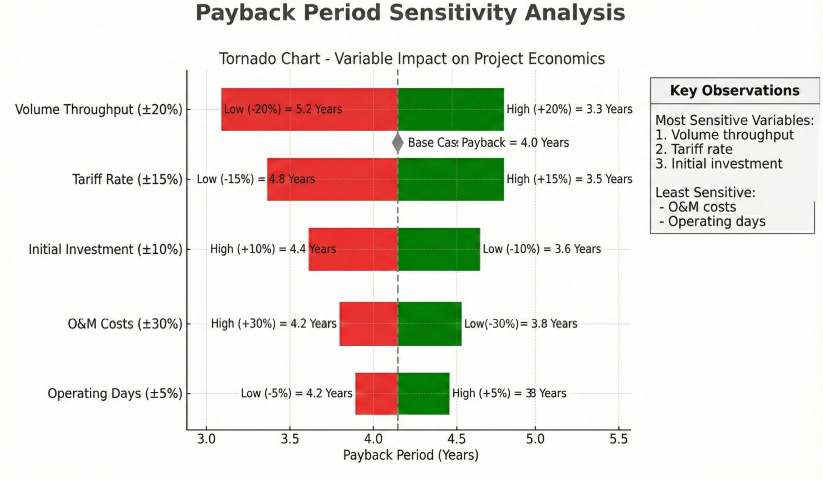

Six-scenario sensitivity table evaluating how payback period changes with key variables:

Scenario

Volume (MMcf/d)

Tariff ($/Mcf)

O&M ($/yr)

Annual CF

Payback (yrs)

Base Case

50

$0.80

$2.0M

$12.6M

3.97

Low volume (-20%)

40

$0.80

$2.0M

$9.68M

5.17

Low tariff (-15%)

50

$0.68

$2.0M

$10.41M

4.80

High O&M (+30%)

50

$0.80

$2.6M

$12.0M

4.17

Optimistic (all favorable)

60

$0.90

$1.8M

$17.91M

2.79

Pessimistic (all unfavorable)

40

$0.68

$2.6M

$7.33M

6.83

Assumes $50M investment, 365 operating days/year

Monte Carlo Simulation for Payback Risk Assessment

For high-value projects, use probabilistic analysis to quantify payback period uncertainty:

Monte Carlo Approach for Payback:

1. Define probability distributions for uncertain variables:

- Volume: Normal distribution, mean 50 MMcf/d, std dev 8 MMcf/d

- Tariff: Triangular distribution, min $0.65, most likely $0.80, max $0.95

- O&M: Log-normal distribution, mean $2.0M, std dev $0.4M

2. Run 10,000 simulations, randomly sampling from distributions

3. Calculate payback period for each simulation

4. Analyze results:

- P10 (10th percentile): 3.1 years (optimistic)

- P50 (median): 4.2 years (expected)

- P90 (90th percentile): 6.8 years (pessimistic)

- Probability of payback < 5 years: 72%

5. Decision: Accept if P90 < management threshold (e.g., 7 years)

Sensitivity tornado chart identifying volume throughput and tariff rate as the most critical variables affecting payback period

Comparison of Investment Decision Metrics

Metric

Advantages

Disadvantages

Best Use

Simple Payback

Easy to calculate; intuitive; emphasizes liquidity

Ignores time value of money; ignores cash flows after payback

Communicate returns to management; compare to hurdle rates

Profitability Index

Measures value per dollar invested; good for capital rationing

Doesn't show absolute value; can conflict with NPV

Budget constraints; ranking projects with different scales

Integrated Decision Framework — 5 Sample Projects

Comprehensive project evaluation using multiple criteria side-by-side:

Project

Investment

Simple PP

Disc. PP

NPV @10%

IRR

PI

Decision

Compressor station

$8M

3.2 yr

4.1 yr

$3.5M

18.2%

1.44

Accept - All metrics favorable

VFD retrofit

$250K

2.8 yr

3.4 yr

$75K

24.5%

1.30

Accept - Excellent returns

Pipeline looping

$40M

6.5 yr

8.9 yr

$2.1M

11.8%

1.05

Marginal - Low but positive NPV

Meter upgrades

$1.2M

8.1 yr

Never

-$350K

7.2%

0.71

Reject - NPV < 0, IRR < WACC

SCADA system

$3M

N/A

N/A

-$1.2M

N/A

N/A

Accept - Safety/reliability, not financial

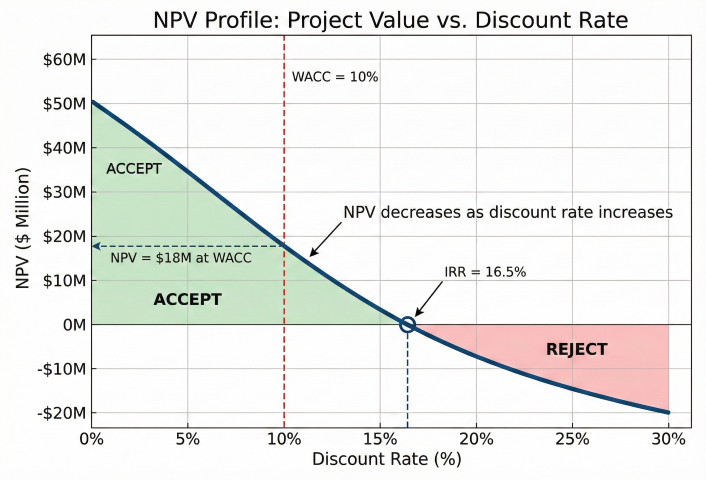

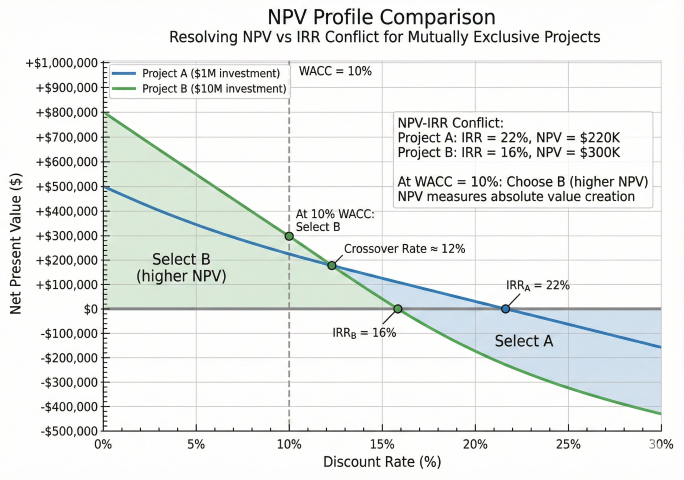

NPV vs IRR Scale Conflict — Worked Example

For mutually exclusive projects of different scales, NPV and IRR can give conflicting rankings:

Example of NPV-IRR Conflict:

Project A (Small):

Investment: $1,000,000

NPV: $400,000

IRR: 22%

Project B (Large):

Investment: $10,000,000

NPV: $2,500,000

IRR: 16%

Analysis:

- By IRR: Select Project A (22% > 16%)

- By NPV: Select Project B ($2.5M > $0.4M)

Correct Decision: Select Project B

NPV measures absolute value creation. Project B adds $2.5M vs. $0.4M.

Even though A has higher percentage return, B creates more shareholder value.

When to use IRR: Comparing projects of similar scale and timing.

When to use NPV: Mutually exclusive projects of different scales (use NPV).

NPV profile crossover chart demonstrating how NPV and IRR can give conflicting rankings for mutually exclusive projects of different scales

Decision Tree for Project Approval (4-Step Process)

Recommended Decision Process:

Step 1: Calculate Simple Payback

- If PP > 10 years → Likely reject (unless strategic)

- If PP ≤ 3 years → Proceed to Step 2 (strong candidate)

- If 3 < PP ≤ 10 → Proceed to Step 2 (requires detailed analysis)

Step 2: Calculate NPV and IRR

- If NPV > 0 AND IRR > WACC → Accept

- If NPV < 0 OR IRR < WACC → Reject

- If NPV ≈ 0 → Sensitivity analysis required

Step 3: Sensitivity and Risk Analysis

- Identify key uncertainties (volume, price, costs)

- Calculate breakeven values

- Assess probability of achieving targets

- Consider strategic value, competitive position, regulatory factors

Step 4: Management Review

- Present all metrics with sensitivity cases

- Recommend accept/reject with rationale

- Identify key assumptions and risks

- Propose monitoring metrics for post-approval tracking

Best practice for combined metrics: Use simple payback for initial screening, NPV as primary decision criterion, IRR for communication to management, and discounted payback for risk assessment. No single metric tells the complete story.

What is the difference between NPV and IRR for midstream project evaluation?+

NPV calculates the present dollar value of all project cash flows at a specified discount rate, while IRR finds the discount rate that makes NPV equal to zero. NPV is preferred for comparing projects of different sizes, while IRR provides an intuitive percentage return for quick screening.

How is WACC calculated for midstream infrastructure investments?+

WACC = (E/V) × Re + (D/V) × Rd × (1-T), where E is equity value, D is debt value, V is total value, Re is cost of equity, Rd is cost of debt, and T is the tax rate. Typical midstream WACC ranges from 8-12% depending on the company's capital structure and risk profile.

What is MACRS depreciation and how does it affect midstream project NPV?+

MACRS (Modified Accelerated Cost Recovery System) allows front-loaded depreciation of capital assets, creating larger tax shields in early years. Midstream assets typically fall under 7-year or 15-year MACRS schedules, and the accelerated deductions improve project NPV compared to straight-line depreciation.

What sensitivity variables have the greatest impact on midstream project NPV?+

The variables with the greatest NPV impact are typically throughput volume (revenue driver), commodity prices or tariff rates, capital cost overruns, operating costs, and discount rate assumptions. Sensitivity analysis should test ±20-30% variation in these key inputs to assess project robustness.

What is Net Present Value (NPV) and how is it used in midstream project evaluation?+

NPV is the sum of all future cash flows discounted to present value minus the initial investment. A positive NPV indicates a project creates value above the required return rate. It is the primary metric for evaluating pipeline, compressor station, and processing plant investments.

What discount rate should be used for midstream pipeline NPV analysis?+

The discount rate is typically the Weighted Average Cost of Capital (WACC), ranging from 8-12% for midstream companies. WACC accounts for the cost of both debt and equity capital. Higher-risk projects may use risk-adjusted rates 2-5% above WACC.

How does project life affect NPV for midstream infrastructure investments?+

Longer project lives increase NPV because more years of positive cash flow are captured. However, distant cash flows are heavily discounted, so most NPV value comes from the first 10-15 years. Typical midstream project evaluations use 15-30 year horizons matching asset useful life.

What is the Profitability Index (PI) and when should it be used?+

PI = PV of cash inflows divided by PV of cash outflows, or equivalently 1 + NPV / Initial Investment. PI > 1 means accept. PI is most useful for capital rationing - when budget is limited, rank competing projects by PI to maximize value per dollar invested.

What is the difference between simple payback and discounted payback period?+

Simple payback divides the initial investment by annual cash flow, ignoring the time value of money. Discounted payback uses present-valued cash flows, producing a longer and more accurate payback period. Discounted payback accounts for the opportunity cost of capital.

What is a typical acceptable payback period for midstream infrastructure projects?+

Midstream companies typically require a simple payback of 2-5 years and a discounted payback of 3-7 years, depending on risk and strategic importance. Pipeline projects with long-term contracts may accept longer paybacks, while wellhead compression typically requires payback under 2-3 years.

Why is payback period alone insufficient for investment decisions?+

Payback period ignores cash flows after the payback date, does not account for the time value of money (simple payback), and cannot compare projects with different cash flow patterns. It should be used alongside NPV and IRR for comprehensive investment evaluation.

How is breakeven analysis related to payback period calculations?+

Breakeven analysis determines the throughput volume, price, or utilization rate at which a project's revenues exactly equal its costs. Combined with payback analysis, it shows both when the investment is recovered and what minimum operating conditions are needed to achieve that recovery.